It seems like people fall into one of two camps: planners and non planners. Whichever side you fall, as an entrepreneur, if you haven’t already discovered, you soon will, planning should be a regular part of running your business.

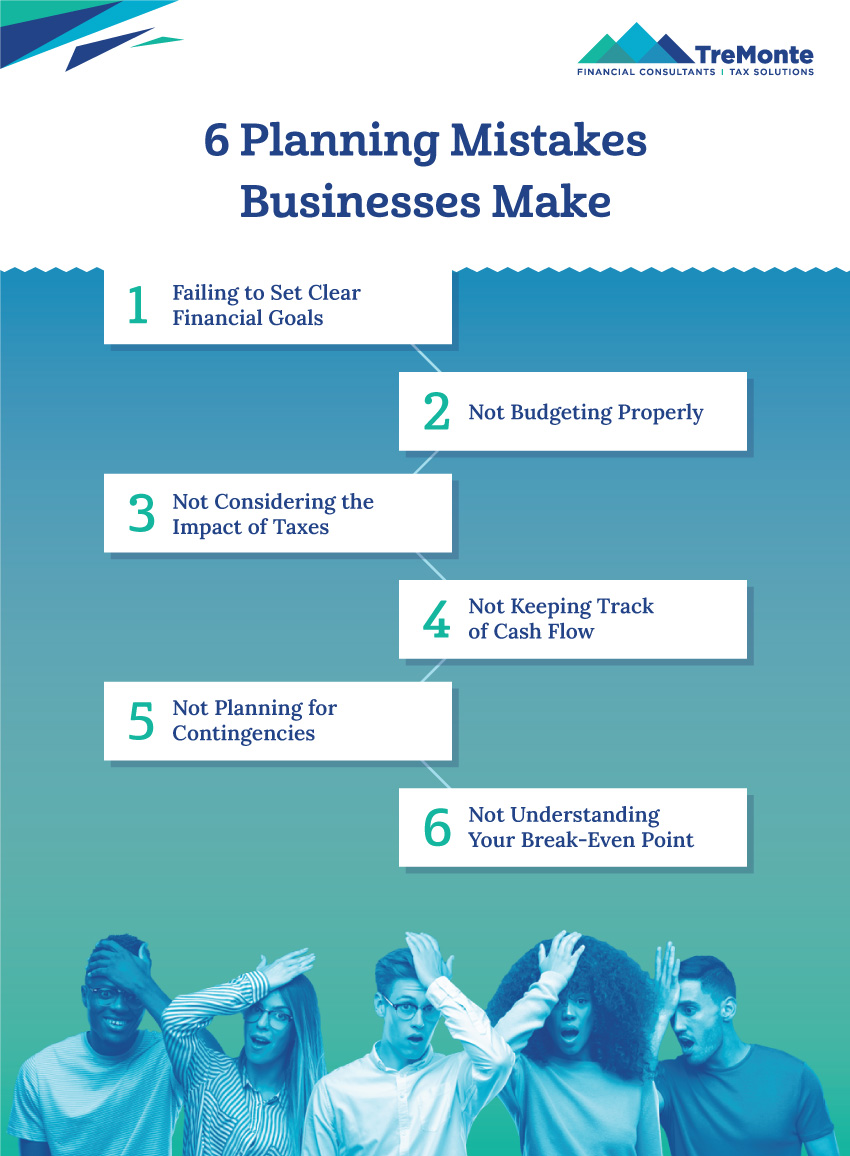

Because we work with business owners regularly, we’ve seen some common mistakes that entrepreneurs make. Here’s a list of six mistakes and why each can be problematic..

1. FAILING TO SET CLEAR FINANCIAL GOALS

Without clear financial goals, it’s difficult to measure the success of your business or to make informed decisions about spending and investments. In order to run a profitable business, you need a roadmap with clear objectives and ways to measure the success of your operations. Enter Key Performance Indicators (KPIs).

KPIs are critical for tracking business goals. They help businesses identify the most important metrics for measuring progress towards objectives, such as sales growth, customer acquisition, and employee productivity. By tracking KPIs, businesses can see whether they are making progress or falling behind and adjust their strategy accordingly.

Keep in mind, goals should be specific, as well. Simply saying “we need to increase revenue” without specifying by how much or in what time frame offers little benefit. Instead say “we will increase revenue by 15% over the next 12 months.” That way, you can measure your progress and adjust your strategy as needed to achieve your goals. Don’t be vague, be specific and track your KPIs to keep your business on the right track.

Speaking of 12 months, you should be setting both short- and long-term goals. Short-term goals can be achieved within a year, while long-term goals focus on the next few years and where you envision your business being in the future.

You can check out our article on SMART Goals for Entrepreneurs for more tips and advice on setting benchmarks for your company.

2. NOT BUDGETING PROPERLY

Business owners often fail to budget properly and end up overspending on certain items, which can lead to financial difficulties.

Budgeting is an essential tool for managing a business’s finances, preventing overspending, and making sure that your business has enough money to cover its expenses.

It’s important to be realistic about the amount of money that will be needed to cover things like rent/mortgage, payroll, inventory, and other operating costs. It’s equally important to be detailed enough that you can avoid surprises as much as possible. Be sure to consider things like marketing and advertising costs, equipment and supply expenses, or other costs that can quickly add up.

Be sure to review and update your business’s budget regularly. Just because you create a budget at the beginning of the fiscal year doesn’t mean it’s etched in stone. Think of your budget as a living, breathing document. Letting it become outdated and irrelevant can make it difficult to manage your expenses effectively.

It’s also important to be aware of the difference between fixed and variable costs. Fixed costs are expenses that remain the same regardless of the amount of product or service produced, for example rent or salaries, whereas variable costs change based on the amount of production, like the cost of raw materials. Having a clear understanding of these costs can help to create a more accurate budget.

3. NOT CONSIDERING THE IMPACT OF TAXES

Taxes can have a significant impact on a business’s bottom line. Accurately estimating your tax liability is crucially important; not doing so can result in unexpected tax bills and penalties when you miss or underpay your quarterly taxes.

Be sure you also take advantage of tax deductions and credits that are available to you and your business. You could save hundreds and even thousands of dollars. A tax professional can help you make sure you’re not missing out on any benefits. They can also help keep you up to date with tax laws which are always subject to change.

Be sure you also consider any state and local taxes that may apply to your business. Different states and municipalities can have different tax laws and rates, and failing to take this into account can result in significant ramifications.

4. NOT KEEPING TRACK OF CASH FLOW

Cash flow is crucial for your business’s survival and growth. Not keeping track of cash flow can mean not having enough money to cover expenses, or missing opportunities to invest in your business’s future.

Make sure you have a clear understanding of the difference between profit and cash flow. Profit is the money left over after all expenses are paid, whereas cash flow is the movement of money in and out of the business. A business can be profitable and still not have enough cash on hand to cover its expenses. Business owners often fail to monitor cash flow on a regular basis, which makes it difficult to anticipate cash shortfalls and take steps to address them.

5. NOT PLANNING FOR CONTINGENCIES

Planning for contingencies is an important aspect of business planning, as it helps businesses anticipate and prepare for unexpected events, such as market changes, natural disasters, and other unforeseen circumstances that can negatively impact the business’s operations and bottom line.

Be sure you have a clear understanding of the risks that your business faces. Without a clear understanding of the risks, it’s difficult to anticipate and prepare your response.

Once you’ve identified your risks, put a plan in place to address those contingencies. Once your plan is in place, it is important to test it to identify any weaknesses, gaps, or areas of improvement so they can be addressed before they become a problem.

6. NOT UNDERSTANDING YOUR BREAK-EVEN POINT

The break-even point is the point at which a business’s revenue is equal to its expenses, and it is important for business owners to understand it in order to make informed decisions about pricing, production, and other aspects of their operations.

You can calculate your break-even point by dividing total fixed costs by the difference between the selling price and your variable costs. It can be easy to not consider all the costs involved in your business’s operations. Doing so may mean you underestimate your break-even point and make decisions that are not financially sound.

Like your budget, you should review your break-even point on a regular basis and adjust it as needed. Consider how changes in production levels will affect your break-even point.

It is important to seek professional advice and guidance in order to avoid these mistakes and have a solid business plan that helps you achieve your goals and grow your business. Tremonte can help you traverse entrepreneurship effectively and successfully. Reach out to us for help with your business’s tax and financial planning needs, and check out our podcast to hear from other entrepreneurs just like you.